About Us

Description of the DITMo® Strategy

DITMo® is a “Buy-Write” portfolio for INCOME employing “Deep-In-The-Money” covered calls. This is a different strategy from typical Covered Call Indexes / Funds. DITMo® Portfolio is devised to mimic the “DITMo® Index” that is an algorithmic representation of a Deep-In-The-Money Buy-Write strategy. Similarly to how one would expect the “XYZ SP500 Fund” to proxy the SP500 Index, DITMo® Portfolio is expected to follow the risk/return metrics of the DITMo® Index. (The DITMo® Index in the “DITMo® Hedge Strategy Monthly” report juxtaposing 20 Hedged Strategies & Indexes is available for free download on http://www.HedgeCo.net/blogs/author/pj)

The DITMo® philosophy is the belief that markets overpay for downside protection from certain equities over the short term.

DITMo® strategy identifies short-term, high probability “relative stability” by creating a portfolio of “Deep-In-The-Money” covered calls that are anticipated to be exercised creating a high yield payoff from option premiums and dividends. DITMo® focuses on one objective: AGGRESSIVE INCOME employing “covered” equities to create a high yield payoff. We believe the optimal risk/return income payoff is created employing Deep-In-The-Money covered calls. Custodians (banks/brokers) allow these covered call strategies in IRAs/ERISA accounts (since the positions are “covered” there is no UBIT exposure). Where the DITMo® strategy differs from typical “At-The-Money” Covered Calls is that ATM Covered Calls (the default strategy of most funds and indexes) – is a “Growth Income” objective whereas, Deep “ITM” objective is 100% Income to have ALL positions exercised (i.e. “Called-Away”) providing an INCOME stream from Option Premiums and Dividends.

DITMo® focuses on only those metrics that determine the likelihood of option exercise to provide an aggressive income.

The guiding principle is to increase probability of option exercise (distinct from the managers of the more common ATM Covered Call Funds). The DITMo® selection metrics include short-term fundamental, statistical and supply/demand measurements. This is the biggest distinction between the DITMo® Philosophy and most other managers that are looking for good long or good short positions.

DITMo® screens for relative stability that is a counter-intuitive selection and “risk- driven” process requiring competencies of a financial risk manager more than a fundamental analyst or a prop derivatives trader. It is a "BUY-HOLD portfolio of approximately 85 Buy-Writes that does not engage in Dynamic Delta Hedging.

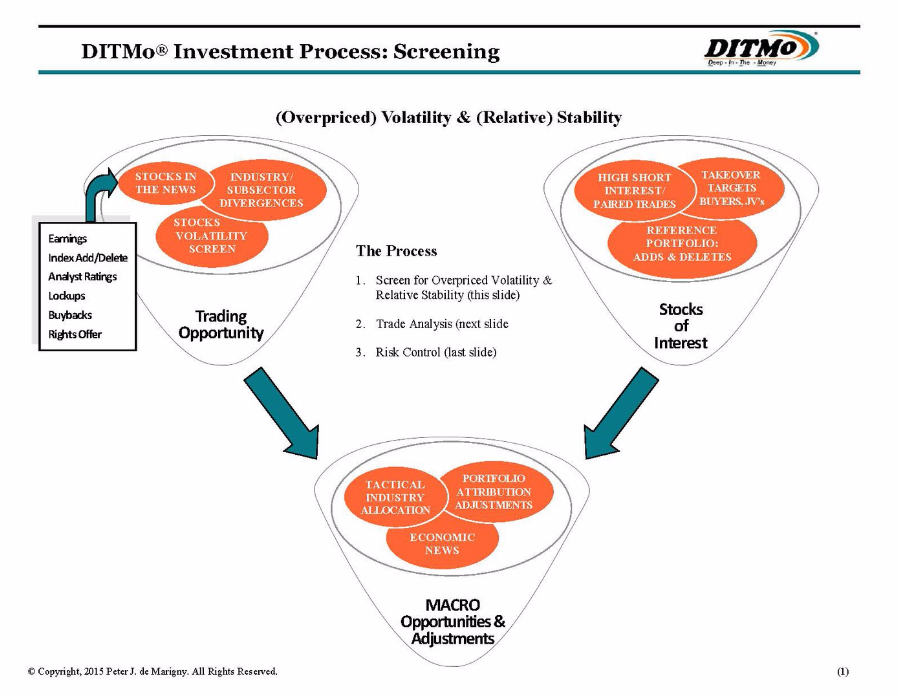

DITMo® Investment Process:

Screening

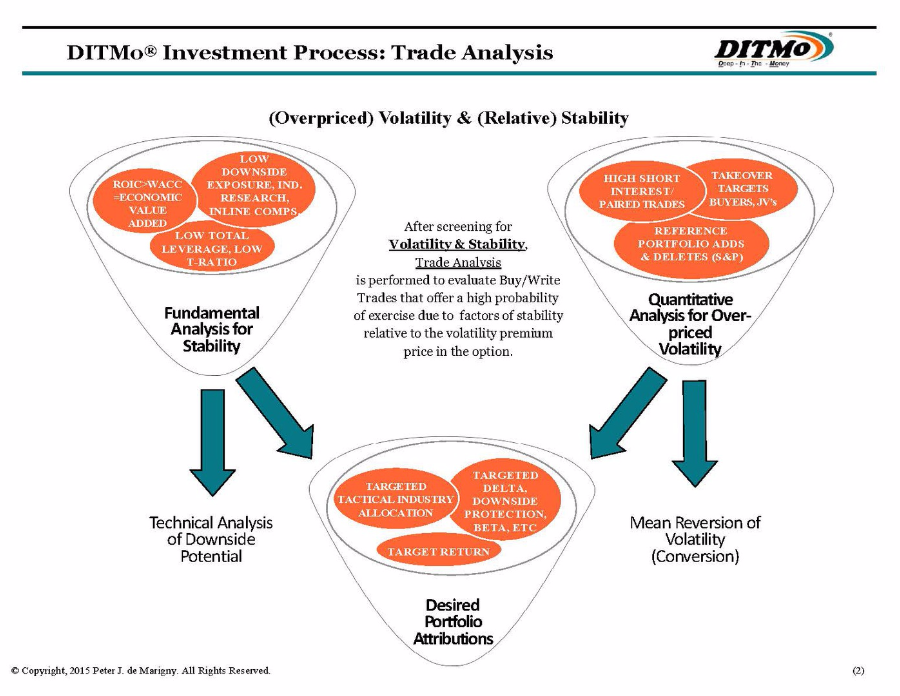

DITMo® Investment Process:

Trade Analysis

DITMo® Investment Process:

Risk Control

This Buy-Write style would categorize DITMo® an “EVENT-DRIVEN” trading style within a “RELATIVE VALUE” classification that is expected to print similarly to DITMo® on a risk/return scatter gram and VAMI Chart. Further characterizing categorization for allocation purposes would include “STAT ARB” as DITMo® screens for distortions in option pricing (i.e. “Implied Volatility”) that provides the downside “cushion” protecting trading profits within a certain range.

Pj does not know of any other managers employing this strategy or investable indexes. Executing a DITM income strategy, unlike many of the other hedge strategies, is found to work best when portfolio management is “RISK-DRIVEN.” That is, the DITMo® portfolio is devised to follow a set of risk metrics using DITM Buy-Writes. This “Risk-Driven” portfolio approach allows DITMo® Portfolio to track the DITMo® Index that is an algorithmic return series based on the SP500. In this way, DITMo® Portfolio can offer a 10Y pro-forma risk/return series similar to how you would expect the Vanguard SP500 to have tracked the SP500.

DITM Covered Calls perform similarly in up, sideways and slightly down markets. Generally, the portfolio will outperform SPX in all conditions except strong up equity markets where DITM is capped in upside at about 12%. DITM Covered Calls utilizing INDIVIDUAL securities (as does DITMo® Portfolio) are not very sensitive to “LOW VOL” environments as DITM Index Calls since even in low VOL environments there are a number of events spiking individual securities offering Buy-Write opportunities of overpriced “relative stability.”

The most challenging environment for DITM Covered Calls is an equity market that experiences most of its gains and losses in very few months or a single quarter. DITM Covered Calls offers a downside “CUSHION” but an egregious drawdown within any single holding period (2-4 months) would not sufficiently cover all losses. The “cushion” is about 1.4 standard deviations in any holding period that is a self-correcting risk control that enlarges in times of high VOL that requires greater downside protection, and conversely, contracts during periods of low VOL that requires a more shallow cushion – but remains a STEADY measure of protection standardized in terms of Standard Deviation.

© DITMo Analytics - Copyright, 2015 Peter J. de Marigny. All Rights Reserved.IONOS MyWebsite